Just a quick note on this morning’s

jobs report. As readers know by now, these pages focus on longer-term developments

in markets and the economic landscape rather than on monthly data. So rather than panning this morning’s dismal

jobs report in isolation, we’ll keep it within the context of the recent trend…..and

the trend in this case, is not our friend.

The Quick & Dirty

August saw nonfarm payrolls

increase by 96,000. Keep in mind that the economy needs to create between

125,000 and 150,000 monthly jobs just to keep up with population growth. Then recognize that nonfarm payrolls are

still 4.3 million lower than they were at the onset of the crisis. Just to reabsorb

those jobs back into the workforce at the creation rate averaged over the past

five months (when the most recent swoon in hiring began), it would take 4.5

years. And don’t forget population growth on top of that. So in order to account

for both of those buckets (new entrants plus the unemployed) the country would

have to average 241,000 new jobs monthly over the next four years. Instead, since

April the average increase has been 84,000 compared to an average of 211,000

over the previous five months (when things actually started looking up…..for a

while). These pages are not political, but any time a politician states that this

rate is anything but abhorrent, try not to laugh in his face or pity them for his

complete lack of understanding of economics.

In addition to the August number

missing its consensus estimate of 130,000, the June and July downward revisions

were 41,000. Moving onto the

unemployment rate, which dropped to 8.1%, that drop is due mainly to 368,000

people leaving the labor force. The broader rate which includes the unemployed

along with those marginally attached to the workforce stands at 14.7%. From

2002 to 2007 this rate averaged 9.1%. Since then it’s averaged 14.9%. Lastly

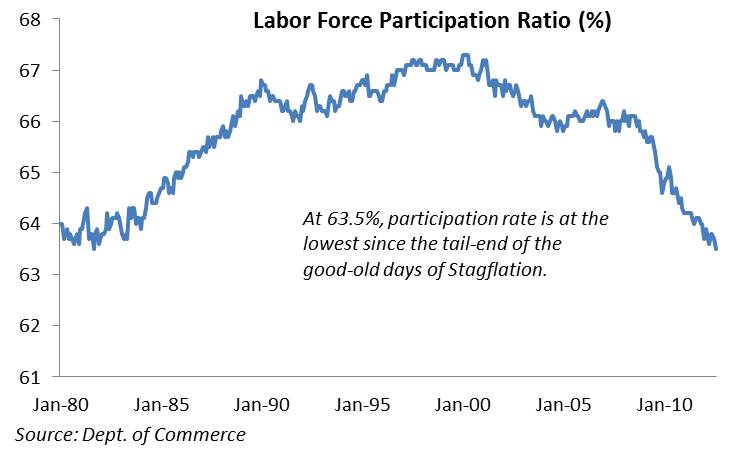

the Labor Force Participation Rate hit a 30-year low at 63.5%, the period the

country sought to shake off the years of stagflation and the Carter-era malaise.

Perhaps the best way to put this

jobs crisis….and it is a crisis…in perspective is to update a favorite chart

from earlier this summer. As seen below, the trajectory of jobs creation in the

current….ahem….recovery, pales in

comparison to anything the country has experienced in decades. Aside from the

obvious personal tragedies of millions of Americans being underemployed or

unemployed, the repercussions for the broader economy are immense. The U.S.

economy is 70% personal consumption. That much of an unemployment overhang

weighs massively on consumer spending. Throw in the ongoing deleveraging of

personal balance sheets, one must ask: how can we fire up the growth machine?

And the Markets

Thursday’s 2% rise in

equities is being attributed to the

extraordinary measures expected to be taken by the European Central Bank to

bring Spanish and Italian borrowing costs down. Investors may have also bid up

shares expecting a weak U.S. jobs report, which would almost cement the

expectation that the Fed would announce future measures in as early as coming

weeks. Question: QE1 and QE2 have done little to ignite jobs growth; why would

another round of easing (at the margins) do any better? Such actions may bid up shares in the short

run but the consequences of such moves cannot be understated. Already the U.S.

dollar has lost ground to the (sickly) Euro, by rising to nearly $1.28 to the

common currency.

No comments:

Post a Comment